A Brief Overview of UBI Literature

A Brief Overview of UBI Literature

Stimulus cheques and enhanced unemployment benefits found in the CARES Act have re-ignited some discussion on the potential need and consequences of implementing a universal basic income. Stimulus cheques, a one time payment with some requirements, and enhanced unemployment, conditional on you losing your job during a global pandemic, have very difference incentives then a permanent universal program. Hence, it’s important to review some literature and arguments on what an actual UBI might actually look like in the real world economy.

There are two common anti-UBI arguments.

1) It would decrease work substantially.

2) It would increase the price of goods substantially.

Both of these are without merit. We still need more evidence to discuss the specific degree of these effects, but current evidence points us in the opposite direction of these claims. I’ll touch on the first point here and the second point in a separate post.

One of the traditional concerns of a UBI is it’s impact on the labour supply - the total hours that workers wish to work at a given real wage rate. Hoynes & Rothstein (2019) go over the effects of various cash programs on the labor supply. They compare basic income trials with related cash transfer programs such as TANF, ACDC and NITs(NITs being similar and sometimes economically equivalent with functional differences). The big takeaway from the paper is that “ongoing UBI pilot studies will do little to resolve the major outstanding questions.” For instance, when analyzing NIT programs, Robins (1985) found substitutions elasticities of around .1-.2 - low for husbands, higher for single women and much higher for married women - and income elasticities around -0.1. The problem with the study is that the program only lasted for a few years so changes may be more reflective of intertemporal substitution than if he program was permanent - intertemporal labor supply elasticities are generally found to be larger than responses to permanent price changes, the estimates responses may overstate the effect of a permanent program.

The Manitoba Canadian UBI trial found a much smaller than expected effect on the labour supply, particularly for married women. A Finnish trial, although limited to people age 25-28, also found no effect, or a slightly negative effect on the labour supply. That being said, there’s a difference between UBI trials and actual permanent UBI programs. Pilot trials have an end date, known to the participants, which is likely to effect their decision processes. These trials are also fairly short and we might see different long run effects when people have the ability to save over time.

The two best unconditional transfer programs we can pull evidence from is the Alaska Permanent Fund (APF) and the Eastern Cherokee Native American Tribe (ECNAT) payments. Jones & Marinescu (2018), analyzing the APF, found no impact on the labour supply. Akee et al. (2010, analyzing the ECNAT payments, also found no impact on the labour supply. The caveat is the relative size of these programs. Many UBI advocates argue for a large payment, maybe one around 10-12k a year to match the poverty line. The APF is around 1-2k a year while the ECNAT is a bit higher at around 3.5-4.5k a year. A more generous monthly UBI might have a larger impact on the labour supply. Something that UBI advocates should note is that although the program in of itself might not have strong labour supply effects, the corresponding taxes required to pay for UBI would. Even if a 2k a year UBI wouldn’t reduce the labour supply, and increase in income taxes to pay for said programs likely will.

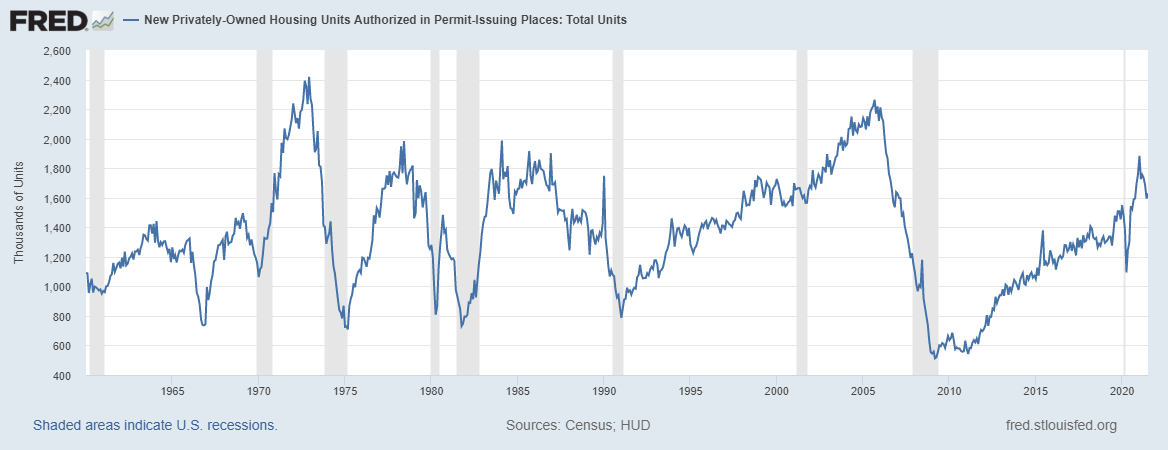

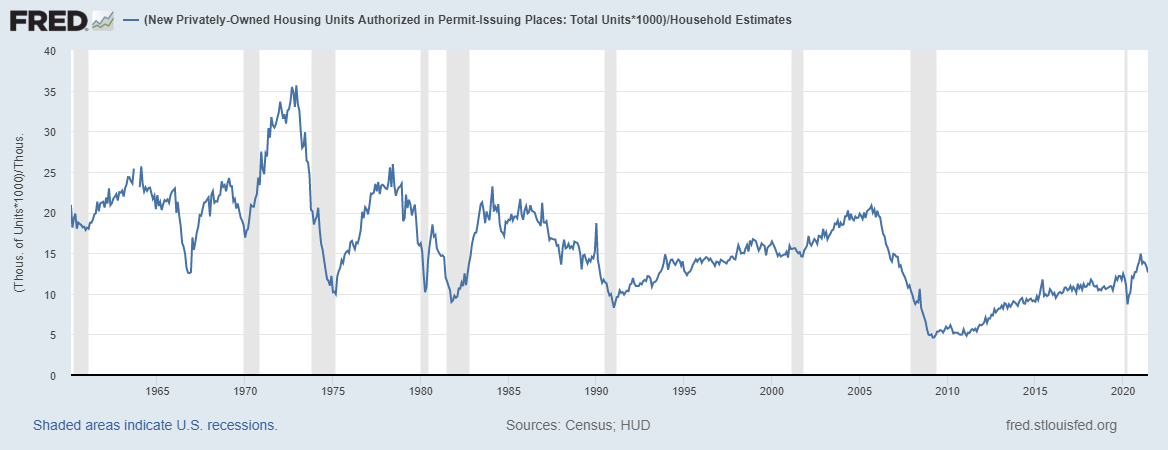

Lastly, I wanted to shortly touch on inflationary impacts without going into too much detail - perhaps for another post. A UBI fully funded by taxes is less likely to have an inflationary impact and the Federal Reserve will play a large role in raining down general prices if any inflation were to occur. People still worry about a key subset of prices, particularly housing and rents. First off, it’s good to ask yourself what’s stopping your landlord from increasing your rent right now? Basic supply and demand would entail sellers wants to maximize their acquired cash and buyers wanting to minimize their lost cash - the real question is centered around a potential increase in the demand for housing. Also, producers still compete with each other. Prices would rise depending on the elasticity - the closer to perfect elasticity, the smaller the increase in prices. This is where things get a little grim. New housing units authorized is quite low, especially when compared to past business cycles. Once you divide the number of units being approved by the number of households than things look even worse. There’s not only less construction compared to normal expansionary cycles, but it’s lower than the amount during past recessions as well. The “good” news is that a lot of housing construction problems are concentrated to specific areas, particularly big cities.

Nonetheless, I still wouldn’t be too worried about inflation and the benefits for most realistic programs would clearly outweigh the cost. But that’s for another post.

I feel like the concerns you mention are around land and capital issues, I've not seen anything directly addressing projections of UBI effects into the future, especially with considerations about capital deepening and automation?